Activity Based Costing - ABC

Description

- An Activity Based Costing (ABC) Methodology represents a structured, automated cost-comparison process, which involves the collection and sorting of cost data associated with the current organization and its activities, and (actual or estimated) cost data associated with the optional delivery mechanisms under consideration.

- ABC allows management to evaluate its organizational efficiency through in-depth reviews of its structure, functions, services, and activities, and therefore provides an organization-wide perspective on opportunities for efficiency: streamlining, work simplification,productivity improvement, more efficient organizational structures, and eliminating duplication and excessive work fragmentation.

When to Use

- ABC can be done at various levels of detail, depending on the objectives of the project. In most cases, only those selected cost items that differ between two options are identified. Comparisons can be carried out at a macro or micro level depending on the size of the organization.

- Cost comparisons can be undertaken only for those services deemed to be a high priority in terms of potential cost savings. Such cost comparisons can be undertaken to estimate potential cost savings of alternative options (e.g. service delivery).

Approach

In general, the cost comparison requires the summarization of cost items, with supporting documentation showing the associated factors and calculations. Frequently, the costing exercise will involve allocating the percentage of time devoted by employees to the activities and tasks carried out by the work unit under review.

There are five main steps:

- Identify mandates, processes and activities.

- Begin the analysis with by identifying the division's purpose as a whole, followed by that of specific sections within the organization.

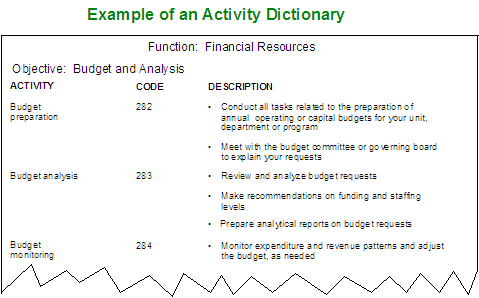

- Develop an activity dictionary.

- Identify the hierarchy of mandates, processes and activities. Present this hierarchy as an "activity dictionary " the cornerstone of an ABC study which is characterized by an unduplicated, all-inclusive list and description of the activities performed by employees. The following are the key components of the activity dictionary:

- Mandates

- Ways of defining an organization's business. They usually represent a macro-grouping of different services or operations within the organization. They answer the question, "Why does the organization exist ?".

- Processes

- Groupings or a sequence of activities carried out to deliver tangible and/or intangible services or final outputs to clients. A process can also be defined as a group of related operations performed to meet a specific client demand or need. Services typically are quantifiable result areas by which the organization measures progress in fulfilling its mandates

- Every organization is unique and has its own set of services, which refer to "What does the organization provide its clients?" Care and foresight should be used to identify services and link these to the processes, as they will be critical in the elaboration of the cost drivers.

- Activities

- Actions that must be taken to provide a service. They may represent a bundling of operations that need to be completed to verbs will be used to introduce all activity descriptions. They answer the question "What does the organization do?"

- Collect time spent by activity.

- Using the "activity dictionary" as a reference manual, ask employees to identify their own activities on a "Work Distribution Form" (WDF) and to indicate the percentage of time they spend on each, thereby accounting for 100 percent of their time. Eventually, each one of these activities is assigned a classification, or "Activity Value" which typically includes four categories called CENO (critical, essential, non-essential and optional according to their primacy to the organization's or work unit's functions).

- Payroll and cost information will also added to the database to determine the cost of each activity to the organization, as well as information on the level of service standards to capture productivity ratios.

- Manipulate data and produce reports.

- Record information from the "Work Distribution Form" into a workstaion (PC):

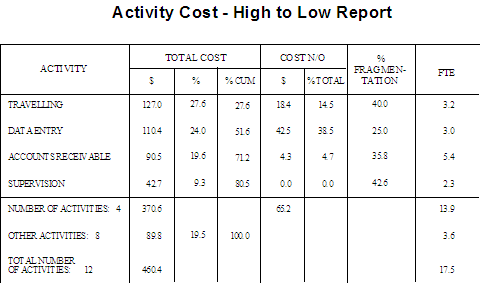

- Activity Cost-High to Low Report: This report lists all activities in descending order of cost to the organization, and also displays the nonessential/optional costs, fragmentation percentage, and number of full-time equivalent staff. The report breaks at the 80 percent point of cumulative cost to illustrate Pareto's Law, which states that 20 percent of the activities generate 80 percent of the costs. This report may indicate, for example, that high-cost activities contribute little value to the organization's missions and/or are highly fragmented.

- Processes: Groupings or a sequence of activities carried out to deliver tangible and/or intangible services or final outputs to clients. A process can also be defined as a group of related operations performed to meet a specific client demand or need. Services typically are quantifiable result areas by which the organization measures progress in fulfilling its mandates. Every organization is unique and has its own set of services, which refer to "What does the organization provide its clients?" Care and foresight should be used to identify services and link these to the processes, as they will be critical in the elaboration of the cost drivers.

- Work Fragmentation Report: This report indicates how many employees are performing an activity, as well as the full-time equivalent number of people required. It develops a fragmentation percentage which indicates the average amount of time that the employees are spending on the activity. The lower the percentage, the higher the degree of fragmentation. The fragmentation ratio shows how many employees' time percentages must be added together to make up one full-time equivalent (FTE). The higher the ratio, the higher the fragmentation. In addition, the report compares total costs.

- Organizational Structure Report: This report indicates the percentage of time that each manager spends in a supervisory capacity and the number of employees directly supervised. By examining the spans of control, time spent supervising and employees supervised, we can assess the necessity of various management positions within an organization.

- Activity Value Report: This report allocates costs and the percentage of time expended to the four activity value categories by work unit and the organization as a whole. The report summarizes and highlights units that have high levels of non-essential or optional costs, indicating the potential for eliminating or reassigning positions. Used primarily as a "red flag", the report directs the analyst to the other reports that will define specific opportunities for improvement in that work unit or organization.

- Work Distribution Report: This report lists every activity performed in the organization, the employees performing the activity, the amount of time they spend on it, the cost of the activity in the organization and the activity's value to the mission of the organization. This report is useful for evaluating where a particular activity is being performed throughout the organization, for example, central agency submissions. This report also lists the organizations and units where the activity is being performed. For many services, these should be located in the same work unit.

- These reports present details of work activities and can be produced by different levels in the organization (e.g. department, section, etc.), showing either individual or consolidated results. Specific groupings can also be made by employee, activity or organizational group according to the organization's particular needs.

- Do a preliminary identification of cost savings opportunities.

- Carry out a careful, systematic review of the reports to identify potential issues, problems and opportunities for cost savings. This analysis will identify:

- Low-priority activities that do not add value to the organization's functions or services

- Overlapping responsibilities or activities duplicated in multiple organizational units

- Activities fragmented among various employees

- Activities performed by an inappropriate work unit or employee level

- Too wide or too narrow spans of control

- Unnecessary management levels

- Inappropriate reporting relationships

- Excessive activity costs

- Excessive number of units

- Managers performing activities that should be performed by subordinates

- Potential for staff reductions or reassignment

- Opportunities for changing methods and procedures.

Guidelines

Problems/Solutions

- Realise that the logistic undertaking for distributing and gathering the forms is immense and can prove to be a prime source of errors.

Tactics/Helpful hints

- Be aware that developing the activity dictionary is one of the most time-consuming tasks and probably one of its most critical since it will directly affect the remainder of the study. The information obtained during this phase consequently needs to be as accurate and as exhaustive as possible. These are the principal sources used for gathering material:

- Consultants sample activity dictionaries

- Existing job descriptions

- Accounting manuals that provide classification plans

- Interviews with client staff

- Company performance measurement systems.

- Since the activity dictionary is a representation of the company's purpose and outputs, its structure is not normally the same as the company's formal reporting hierarchy. As well, many activities will not be contained within a given department or unit. Keep the following in mind when assembling an activity dictionary:

- Objectives should be as quantifiable as possible.

- Activities should cover everything done in a company but should not overlap. They should be mutually exclusive and collectively exhaustive.

- Verbs should be used to introduce all activity descriptions.

- Number each function, service and activity, according to activity dictionary guidelines. Rigorously respect the numbering system as it will be used in the data-entry phase.

- When assigning codes to activities, note that the numbers 001 to 010 are reserved for activities defined as supervisory in nature. Identify these activities beforehand, and include activities related to direct supervision.

Examples

No comments:

Post a Comment